Fixed vs. Variable Expenses: The Budget Breakdown That Actually Makes Sense

Budgeting sounds boring, but here's the thing: understanding your money is actually the key to having more freedom, not less. And it all starts with understanding two types of expenses: fixed and variable.

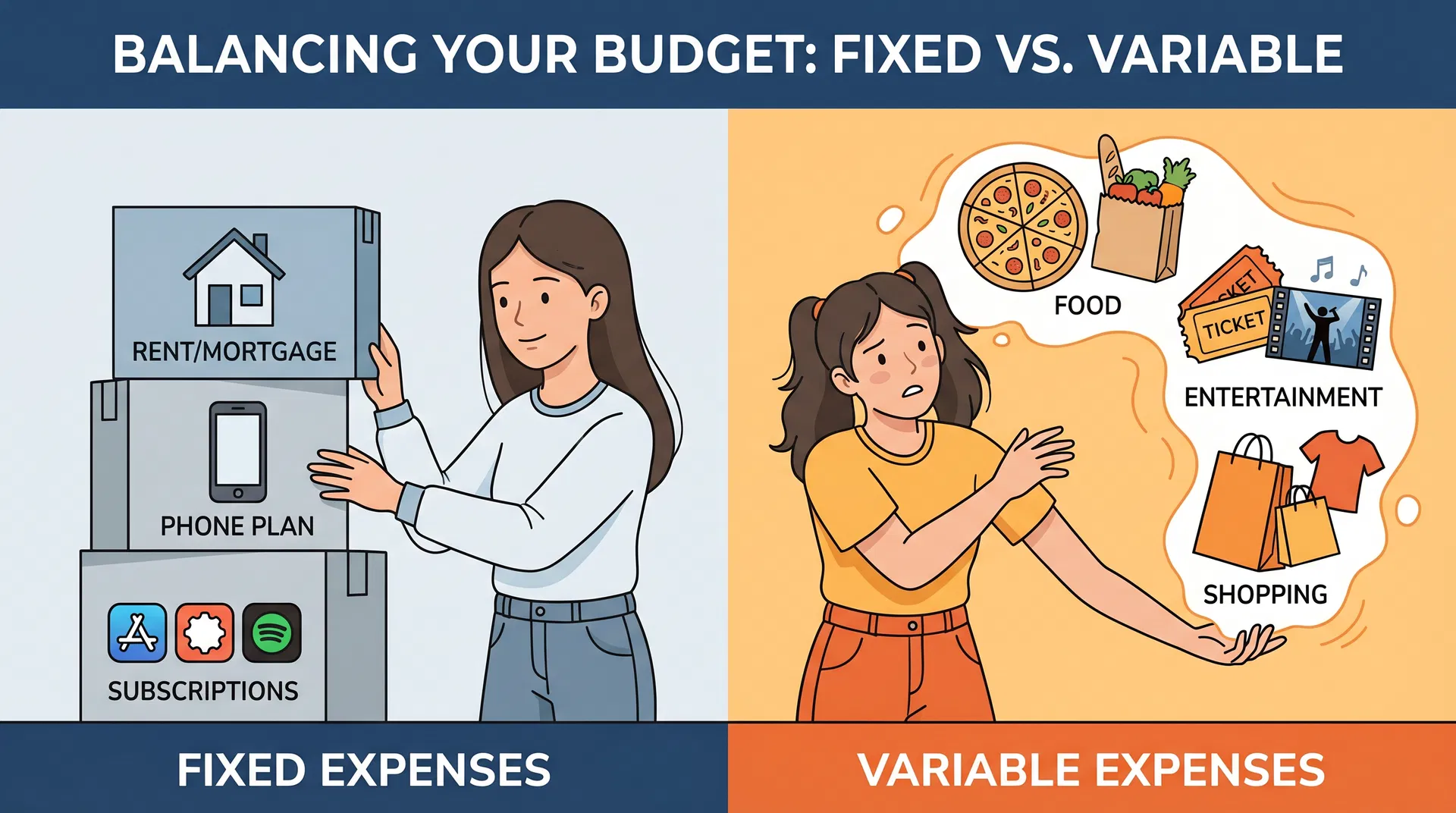

What Are Fixed Expenses?

Fixed expenses are costs that stay the same every month. They're predictable and reliable (which is both good and bad). Examples include:

- Rent or mortgage (if you're paying it)

- Insurance (car, health, etc.)

- Phone bill

- Subscription services (Netflix, Spotify, etc.)

- Gym membership

- Student loan payments

The cool thing about fixed expenses is that you know exactly what they'll be. You can plan around them. The tricky thing is that they're hard to change quickly if you need to cut back.

What Are Variable Expenses?

Variable expenses change from month to month. They're the flexible costs that depend on your choices and circumstances. Examples include:

- Groceries (you might buy more or less depending on what you need)

- Gas (prices fluctuate, and you drive different amounts)

- Dining out

- Entertainment (movies, concerts, games)

- Clothing

- Gifts

- Fun activities

Variable expenses are flexible—you can control them more easily. If money is tight, you can eat out less or skip the new video game. But because they change, they're harder to predict.

Why Does This Matter?

Understanding the difference helps you budget smarter. Here's why:

Fixed expenses are your baseline.

These are the costs you HAVE to pay. If your fixed expenses are $500 per month, you need to make at least $500 to cover them. Anything beyond that can go toward variable expenses, savings, or fun.

Variable expenses are where you have power.

Since they change, you can adjust them based on your goals. Want to save for something? Cut back on variable expenses. Need more breathing room? Look for ways to reduce variable costs without sacrificing quality of life.

A Real Budget Example

Let's say you're a teen with a part-time job earning $400 per month:

Fixed Expenses:

• Phone bill: $50

• Subscriptions: $20

• Total fixed: $70

Variable Expenses:

• Dining out: $80

• Entertainment: $60

• Clothing: $40

• Savings goal: $100

• Total variable: $280

Total spending: $350

Left over: $50

In this example, your fixed expenses are small, so you have flexibility with variable expenses. But notice how the person allocated $100 to savings—that's intentional. They're not just spending whatever's left; they're being strategic.

The Strategy

Here's the budgeting hack: prioritize your fixed expenses first, then allocate your variable expenses, then save whatever's left. Or even better: save first, then spend what's left.

The key is being intentional. Every dollar should have a purpose. Some go to necessities (fixed), some go to wants (variable), and some go to future-you (savings).

Pro Tip

As you get older and earn more money, watch your fixed expenses. They tend to creep up. A bigger apartment, a car payment, insurance—these add up. The more fixed expenses you have, the less flexibility you have. So when you're young and have few fixed expenses, that's the time to build good savings habits and invest. Future-you will thank you.

Written by: ZalaSmart Team

Teaching children and youth the essential life skill of financial literacy.